How Long Does Bankruptcy Stay on Your Record?

If you filed for bankruptcy or are considering it, you are probably wondering how long it will remain on your credit report.

The answer depends on the type of bankruptcy involved. Federal law sets clear limits on how long bankruptcies may be reported and provides legal remedies if those limits are exceeded.

Below, you will see how long Chapters 7, 11, and 13 can appear on a credit report, when the reporting period begins, and what steps may be available if a bankruptcy is reported longer than the law permits.

How Long Does Bankruptcy Stay on Your Record?

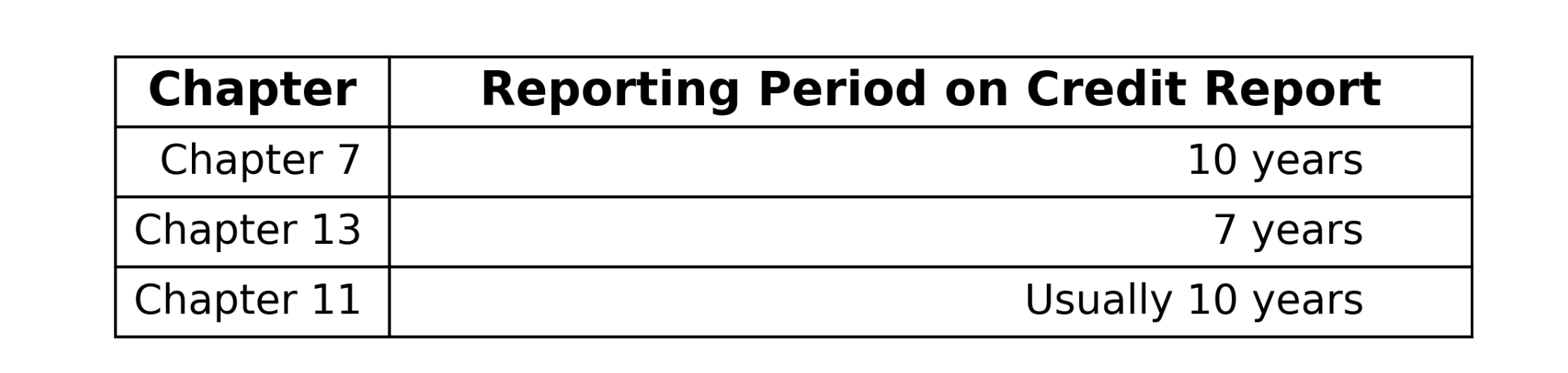

The federal law that regulates credit reporting time limits is the Fair Credit Reporting Act, or FCRA. Under the FCRA, bankruptcies may remain on your credit report for 7 to 10 years, depending on the type filed.

The reporting period generally begins on the date the bankruptcy was filed, not the date it was discharged. That distinction matters. Here is the general timeline:

Chapter 7: Up to 10 years from the filing date

Chapter 13: Up to 7 years from the filing date

Chapter 11: Usually up to 10 years from the filing date

These time limits apply to consumer credit reports furnished by the three major credit bureaus, Experian, TransUnion, and Equifax, as well as other consumer reporting agencies.

However, bankruptcy cases may appear in other types of records for longer periods of time. For example, federal court dockets and public record databases may retain bankruptcy filings indefinitely.

Another example involves employment background checks, which are generally subject to the same FCRA time limits. However, for certain high income positions, typically those with an annual salary of $75,000 or more, the FCRA may permit the reporting of bankruptcies for longer than the standard time limits.

How Long Does a Chapter 7 Stay on Your Record?

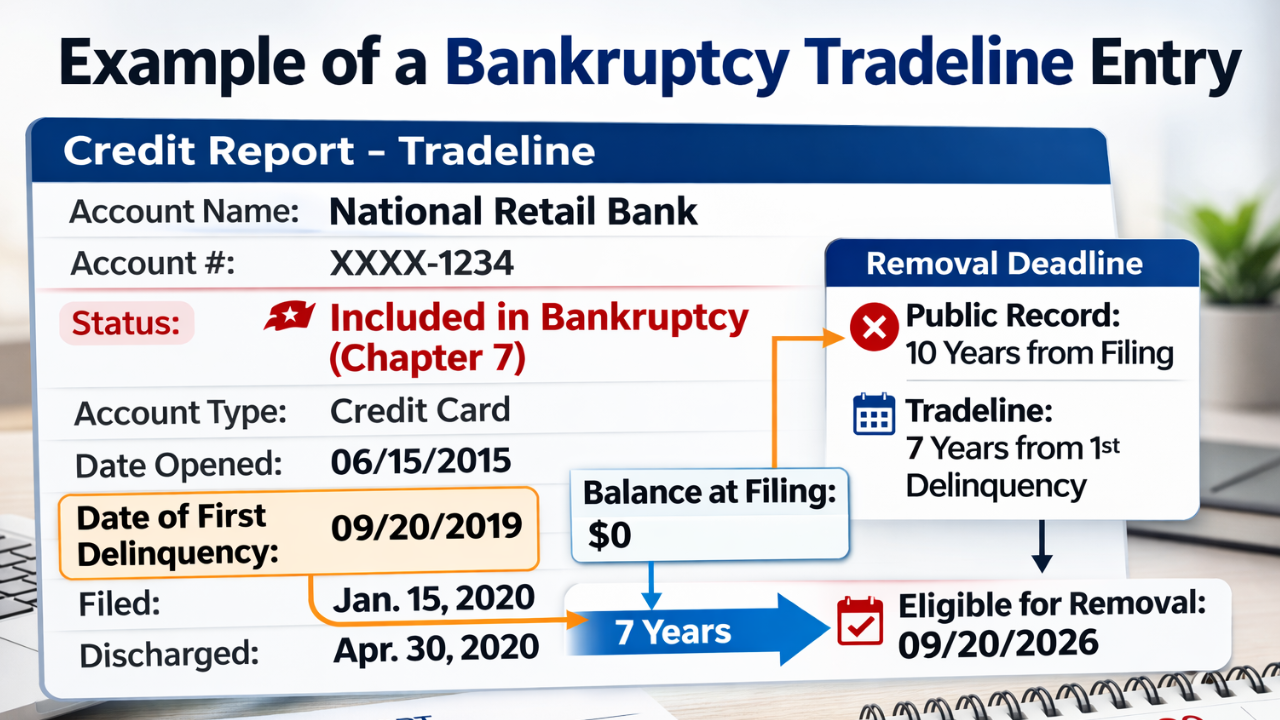

A Chapter 7 bankruptcy may remain on your credit report for up to 10 years from the filing date. That 10 year period applies to the bankruptcy public record itself. It does not automatically apply to every account that was included in the bankruptcy.

Credit reports typically reflect bankruptcies in two ways. The first is through a public record entry. This is information gathered from federal court records showing that a bankruptcy case was filed. That public record may remain on a credit report for up to 10 years from the filing date.

The second way bankruptcies appear is at the account level, often called a tradeline. These entries show each of your current and past credit accounts and are reported by your creditors to the credit bureaus. A bankruptcy notation will usually appear on each account that was discharged. In most cases, these accounts may not be reported for more than 7 years from the date of first delinquency that led to the account’s charge off or collection.

This means many of the individual debts included in a Chapter 7 case may fall off your credit report before the bankruptcy itself does.

For example, if a credit card first became delinquent in January 2018 and you filed Chapter 7 in June 2019, that account will typically fall off around January 2025, even though the bankruptcy public record may remain until 2029.

Because these reporting clocks run independently, it is common to see individual accounts disappear several years before the Chapter 7 notation is removed.

How Long Does Chapter 13 Stay on Your Record?

A Chapter 13 bankruptcy is commonly reported on a credit report for 7 years from the filing date.

Although the FCRA permits bankruptcies, including Chapter 13 cases, to be reported for up to 10 years, the major credit bureaus typically limit Chapter 13 reporting to 7 years as a matter of industry practice.

The reporting period begins when the case is filed and is not reset simply because the case is later dismissed, converted, or completed. The original filing date controls the timeline.

How Long Does Chapter 11 Bankruptcy Stay on a Credit Report?

A Chapter 11 bankruptcy may be reported on a credit report for up to 10 years from the filing date.

Chapter 11 is most commonly used by businesses, but individuals may file under Chapter 11 in certain circumstances. For credit reporting purposes, it is treated like other bankruptcy cases under federal law.

As with other chapters, the reporting period begins when the case is filed. The bankruptcy public record may remain for up to 10 years, while individual accounts included in the case are generally subject to their own 7 year reporting timelines tied to the date of first delinquency.

What If a Bankruptcy Stays on Your Record Too Long?

If a bankruptcy remains on your credit report beyond the legal time limit, that may violate the FCRA.

The first step is usually to submit a written dispute to the credit bureau reporting the information. Your dispute should clearly identify the bankruptcy entry, explain that it is being reported beyond the permitted timeframe, and request correction or removal.

After receiving a dispute, the credit bureau is required to conduct a reasonable investigation. If the bankruptcy is inaccurate or outdated, it must be corrected or deleted.

If you notice that a bankruptcy is still appearing on your credit report after the reporting period has expired, contact my office to discuss your situation. I can evaluate whether the reporting may violate the FCRA and advise you on the options available to you under federal law.