How Long Does an Eviction Stay on Your Credit?

In most cases, an eviction can affect your record for about seven years. But it’s important to understand that eviction-related information can appear in several different places.

For example, an eviction may appear on tenant screening reports used by landlords, in public court records, or sometimes on a credit report if unpaid rent is sent to collections. Each of these reporting systems follows different rules, so it’s important to identify where your eviction history is actually showing up.

Problems can arise when one of these reporting systems continues reporting eviction information longer than it should, or reports it inaccurately. When that happens, federal law may give you the right to dispute the information and potentially recover monetary damages if a reporting company violates the law.

How Long Does an Eviction Stay on Your Credit?

The first place eviction history can show up is on your credit report. For this section, “credit report” refers to reports generated by the three main national credit bureaus: Experian, Equifax, and TransUnion.

The federal law that governs how long information can stay on your credit report is the Fair Credit Reporting Act, or FCRA. There are two ways eviction-related information or negative rental history can appear on a credit report.

The first is through eviction judgments that appear in the public record section of a credit report. However, the major credit bureaus stopped reporting most civil judgments several years ago as part of industry changes intended to improve the accuracy of public record reporting. As a result, eviction cases filed in court typically do not appear directly on modern credit reports.

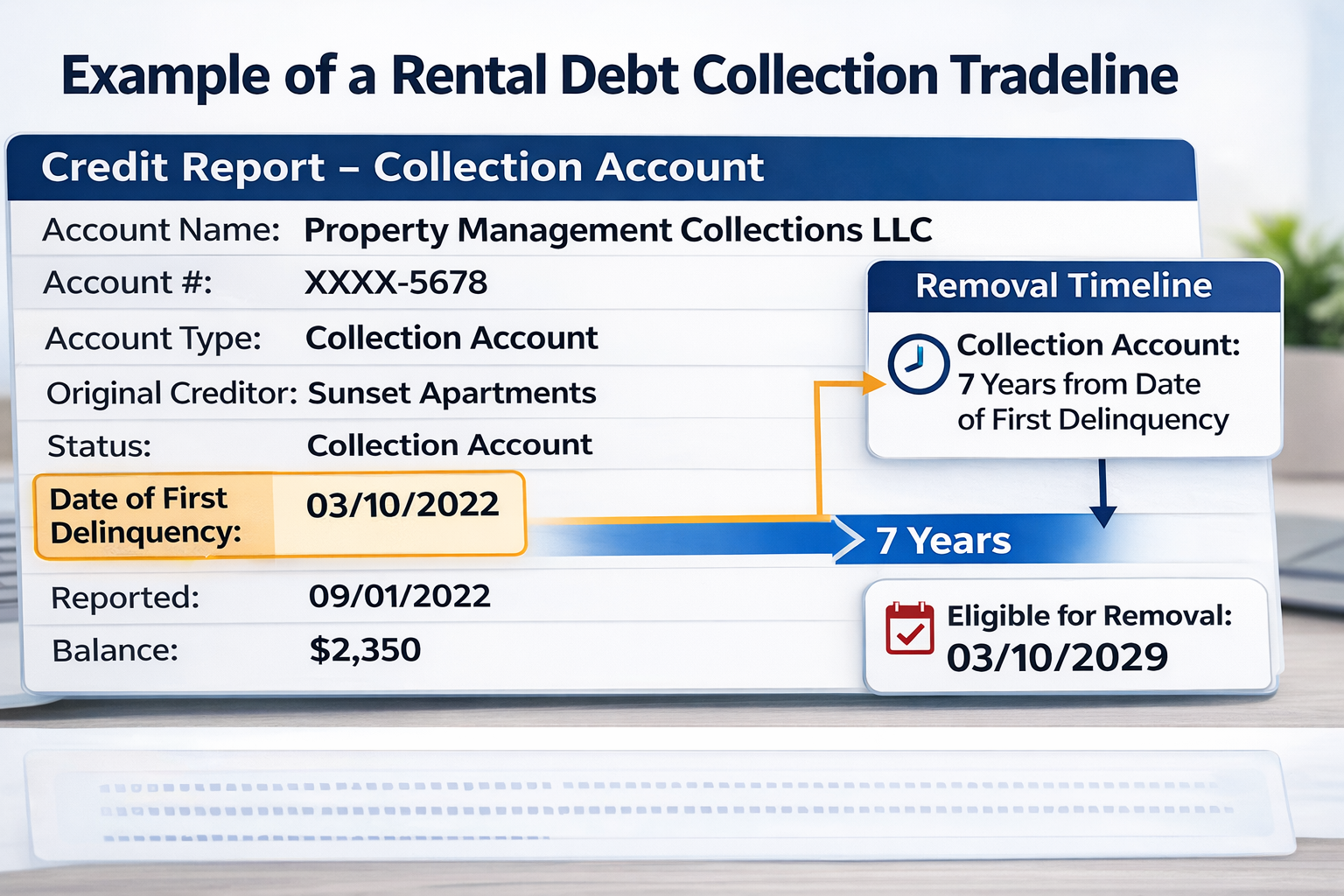

The second, and more common, way eviction-related information may show up on your credit report is when a landlord sends an unpaid balance to a debt collector. The collector may then report the debt to the credit bureaus, where it can appear on your credit report as a collection account or other negative item.

When rental debt is reported in this way, the FCRA generally allows it to remain on your credit report for up to seven years. While this type of negative item can affect your credit score and your ability to qualify for a new apartment, credit reports are not the primary way landlords check eviction history.

How Long Does an Eviction Last on Your Record?

Instead of credit reports, landlords and property managers often rely heavily on tenant screening reports when evaluating rental applicants.

Tenant screening reports are similar to background checks, but they are designed specifically for rental housing. Landlords use these reports to review information about an applicant’s rental history, which may include prior eviction filings, eviction judgments, and other housing-related court records.

The information on these reports are subject to the same FCRA timeline reporting limits as regular credit reports. This means that any negative information on a tenant screening report can generally only be reported for seven years.

How Long Does an Eviction Stay on Your Rental History?

In addition to tenant screening reports, eviction-related information may also appear in rental history databases used by property managers and large apartment complexes. These systems track information about prior tenancies and may include records related to unpaid rent, lease violations, or eviction filings.

In some cases, property managers share information through industry databases or screening platforms that allow landlords to review an applicant’s prior rental behavior.

Unlike tenant screening reports, the reporting limits for some private rental history databases are less clear. In some cases, information in these systems may not be subject to the same seven-year reporting limits that apply to credit reports and tenant screening reports under the FCRA.

What If an Eviction Is Still Showing?

Eviction-related information that continues to appear on your credit report or tenant screening report after the seven-year reporting limit may violate the FCRA. In that situation, you generally have the right to dispute the information. If the credit bureau or screening company continues to report the outdated information after your dispute, you may have the right to file an FCRA lawsuit against them.

Wherever you are in this process, it can be helpful to have an experienced consumer protection attorney on your side. Reach out to my office to discuss your situation and I will let you know what legal options may be available under the FCRA.