How to Remove a Repossession from Your Credit Report (When It’s Actually Possible)

A repossession on your credit report can have a serious impact. So it’s only natural to want to get it removed.

But in most cases, a repossession won’t be removed just because it’s hurting your credit. There needs to be a valid legal basis for the credit bureaus to remove it.

In this article, I’ll explain what federal law actually says about repossessions and how to use those rules to your advantage.

Can a Repossession Be Removed from Your Credit Report?

The federal law that governs credit reporting is the Fair Credit Reporting Act (FCRA). Under the FCRA, credit bureaus and the companies that furnish information to them are required to ensure that the information on your credit report is accurate.

Accuracy is the key. If your repossession is being reported correctly and is not misleading, getting it removed will usually be an uphill battle.

If the repossession is being reported inaccurately, however, you have the right to dispute that information with the credit bureaus. This is the first step in enforcing your rights under the FCRA.

If the issue is not corrected after your dispute, you may have the right to bring a claim under the FCRA. In that situation, the law allows for both correction of the error and, in some cases, monetary damages depending on the circumstances.

When a Repossession Can Be Removed (Errors That Matter)

What qualifies as an inaccuracy under the FCRA is more expansive than most people think. Even if your car was actually repossessed, the way it is reported can still be incorrect.

Here are some of the most common issues to look for:

Incorrect balance after the vehicle was sold: After a repossession, the vehicle is typically sold and the proceeds are applied to the loan. If the remaining balance is reported incorrectly, that can be a problem.

Duplicate tradelines: The same repossession should not appear multiple times as separate accounts. Duplicate reporting can make the situation look worse than it actually is.

“Past Due” balance after payment: If you paid off the remaining balance, the account should reflect a $0 balance. Continuing to report a past due amount may be inaccurate.

Account still reported as open: A repossession usually means the account is no longer active. If it’s still being reported as open, that may be inaccurate or misleading.

Incorrect dates: Dates matter for how long a repossession can remain on your credit report. If the timeline is wrong, it may affect how long the account is reported.

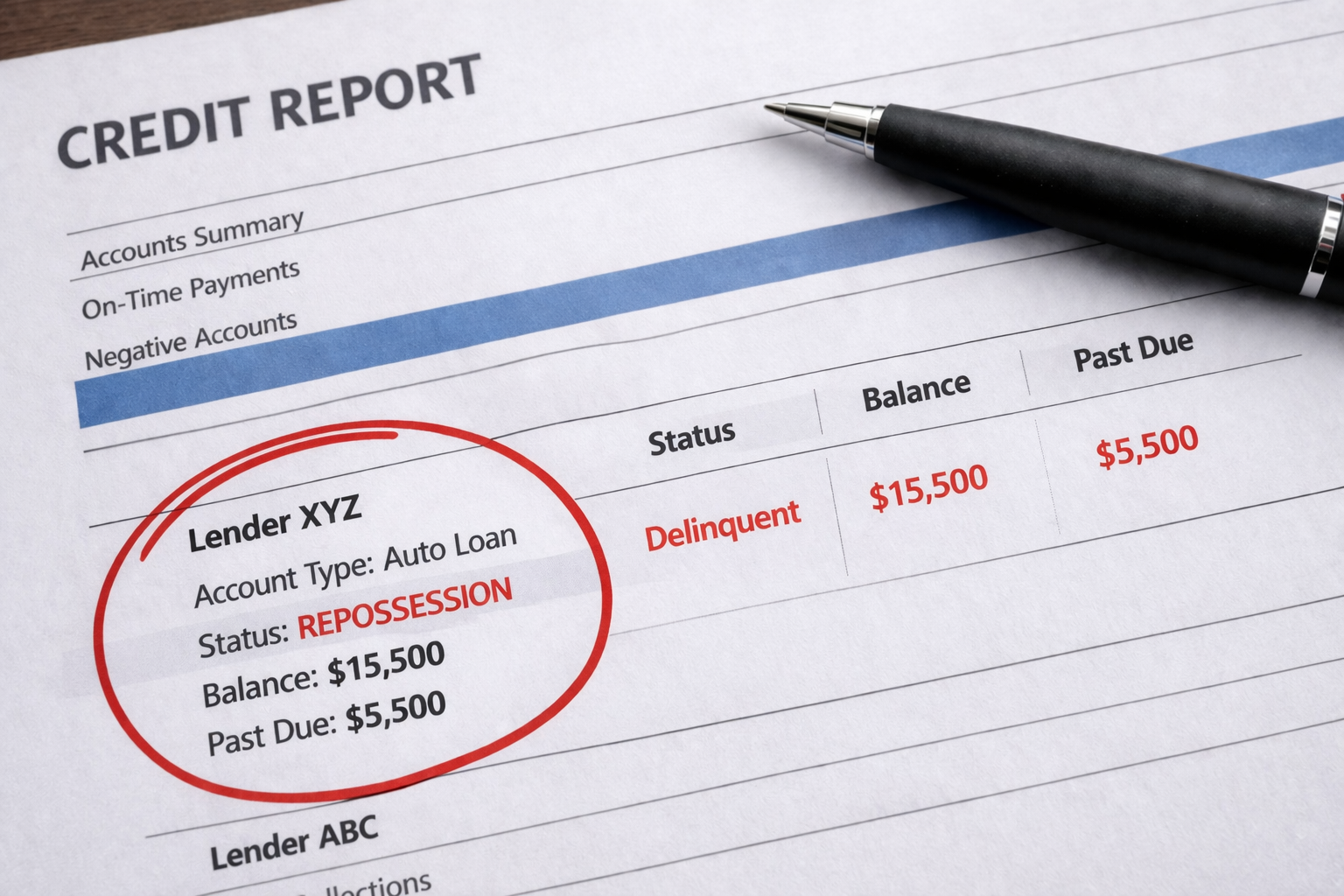

Wrong status or marks: Repossession accounts are sometimes reported with statuses such as “collections,” “delinquent,” or “30 days late.” These designations must accurately reflect the current status of the account. If they do not, that can be a reporting issue.

Repossession obtained illegally: If your vehicle was taken without a legal right to do so—for example, if you were not actually in default or the wrong car was repossessed—that may go beyond a credit reporting issue. In those situations, the repossession itself may be unlawful, and any related credit reporting can also be challenged.

In most of these examples, the issue is not whether a repossession occurred, but whether the details are being reported accurately. If they are not, the first step is to dispute the information with the credit bureau reporting the error. In some cases, this leads to a correction rather than a full removal, meaning the repossession may remain on your credit report but must be reported accurately.

How to Get a Repossession Off Your Credit Report

As mentioned earlier, the first step in removing a repossession from your credit report is disputing the information with any credit bureau that is reporting it. Although there are multiple ways to submit a dispute, including online or by phone, sending a physical letter is often the strongest approach.

A written dispute creates a clear paper trail of your attempt to correct the inaccuracy. If the credit bureaus fail to fix the issue, you have a record showing that you took the required steps under federal law. That can strengthen a potential claim under the FCRA if you choose to pursue it.

Your dispute letter should clearly explain what is inaccurate about the repossession and request that the information be corrected or removed. If you’re not sure how to structure your letter, I provide a free repossession dispute letteron my website that you can use as a starting point and tailor to your situation.

After your dispute is submitted, the credit bureaus generally have 30 days (plus a few days for mailing) to investigate. During that time, they will contact the company that furnished the information and determine whether the account should be updated, removed, or verified.

If the issue is corrected, the repossession may be updated or removed depending on the nature of the error. If the inaccurate information is verified and remains on your report, that may be where legal options come into play.

How to Remove a Voluntary Repossession from Your Credit Report

A voluntary repossession does not change how the account is treated for credit reporting purposes. Even if you returned the vehicle yourself, it is still reported as a repossession and will have a negative impact on your credit.

The same rules apply here. A voluntary repossession can only be removed if there is an issue with how it’s being reported. If the information is accurate, it will typically remain on your credit report for up to seven years.

That said, voluntary repossessions can still involve reporting errors. The balance may be incorrect after the vehicle is sold, the account status may not be updated properly, or other details may be inaccurate. If that happens, you may have grounds to dispute the reporting and request that it be corrected or removed.

How to Remove a Redeemed Repossession from Your Credit Report

A redeemed repossession means you were able to bring the loan current and get the vehicle back after it was repossessed. While the repossession event may still be reported, the account should reflect what actually happened after the redemption.

This is where reporting issues often arise. In some cases, the account may still be reported as a repossession without showing that the loan was reinstated. In others, the balance, status, or payment history may not be updated correctly.

When that happens, the issue is not the repossession itself, but how the account is being reported after the fact. If the reporting does not accurately reflect the redemption, you may have a valid basis to dispute the information and request that it be corrected.

Can Credit Repair Companies Remove Repossessions?

Credit repair companies often claim that they can remove negative items like repossessions from your credit report. But in reality, they do not have any special authority to remove accurate information.

A repossession can only be removed if it is being reported inaccurately. Credit repair companies use the same dispute process that is available to you—they are not able to override accurate reporting simply because it is damaging to your credit.

This includes well-known companies like Lexington Law. While they may assist with organizing and sending disputes, the outcome still depends on whether there is an actual reporting issue.

It’s also worth noting that credit repair companies are regulated under the Credit Repair Organizations Act (CROA). Among other things, CROA prohibits these companies from making misleading claims about what they can achieve and requires certain disclosures about their services.

When a Repossession May Lead to a Legal Claim

If your dispute does not correct inaccurate information on your credit report, you may have the right to bring a claim under the FCRA against the credit bureaus and, in some cases, the company reporting the information.

An FCRA claim can result in correction or removal of the inaccurate repossession. You may also be able to recover monetary damages, and if your claim is successful, the law allows you to recover your attorney’s fees.

If you’re dealing with an inaccurate repossession on your credit report and your disputes are being ignored, you can reach out to my office for a free consultation. I’ll review your situation and let you know what options may be available to you under the FCRA.